Where Do Banks Get Their Money From To Led To People For Loans

Banks' Funding Costs and Lending Rates

Download the complete Explainer 207KBBanks' funding costs and lending rates are an of import part of the manual of monetary policy to economical activity and ultimately inflation (see Explainer: The Manual of Budgetary Policy). The interest rates that banks charge borrowers and pay to savers influence the decisions of businesses and households about how much they desire to borrow or salve. To fully understand the transmission of budgetary policy, it is of import to empathise what banks' funding costs and lending rates are, and what influences them.[1]

What are Banks' Funding Costs and Lending Rates?

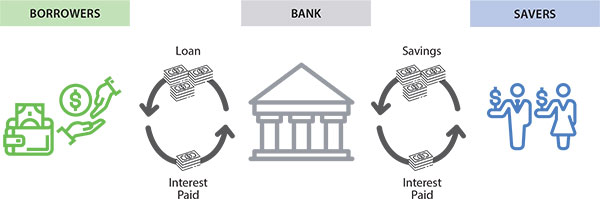

Banks collect savings from households and businesses (savers) and apply these funds to make loans to those who want to infringe (borrowers). Banks must pay interest on the funds that they collect from savers, which is one of their main funding costs. On the other paw, banks receive interest from loans that they make to borrowers and this is a large part of their revenue. From the perspective of a bank:

- funding costs are the involvement rates paid to savers

- lending rates are the involvement rates paid by borrowers.

How do Banks Fund Themselves?

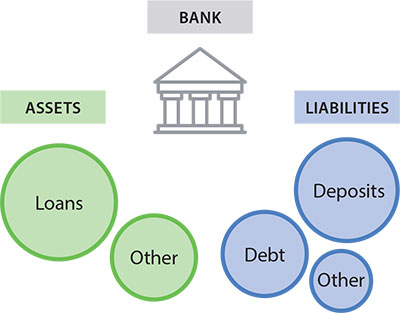

Banks collect funds from savers in various means. Deposits from Australian households and businesses account for just over half of Australian banks' total funding. Banks can as well collect funds from savers by issuing bonds and other debt securities in financial markets, which account for around a third of Australian banks' funding. Other sources of funding like equity – for example, banks' shares listed on the share market place – correspond the residual of banks' funding. (For updated information on the composition of funding for banks in Australia, run across the Reserve Bank'southward monthly Chart Pack.)

What Influences Banks' Funding Costs?

The cash rate

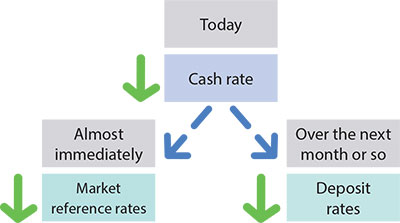

The cash rate has an important role in determining the involvement rates on banks' funding sources. However, the interest rates banks pay for dissimilar sources of funding don't necessarily move by the same amount or at the same speed as a change in the cash rate.

Marketplace reference rates

Changes in the cash rate are typically transmitted quickly to an important group of interest rates called 'market place reference rates'. Market place reference rates are based on transactions between participants in a financial market that happen often enough to reliably measure these rates. Because market place reference rates are reliably measured, they are often used equally a benchmark for pricing bonds and other debt securities, including those issued by banks. An example of an of import marketplace reference rate for bank funding costs is the bank bill swap charge per unit (BBSW).

Deposit rates

Deposit rates are less directly influenced past the cash rate and changes to the cash rate also tend to take some time to be transmitted to deposit rates. This is because banks take discretion in setting deposit rates and also considering deposit rates are influenced past other factors. For example, banks may raise eolith rates, independently of a modify in the greenbacks rate, to concenter more deposits. Banks might wish to hold more than deposits considering they are considered more stable than some other sources of funding.

Other monetary policy tools

Other monetary policy tools can likewise have implications for banks' funding costs (see Explainer: Unconventional Monetary Policy).

Extended liquidity operations: term funding schemes

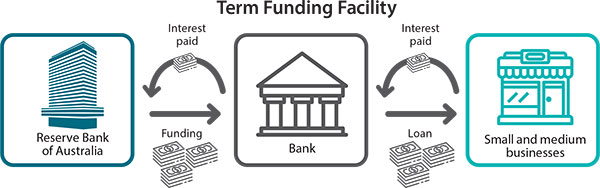

Term funding schemes let banks to borrow funding from the central banking concern at a depression cost for an extended menstruation. These schemes aim to lower banks' funding costs and provide funding that is stable, particularly in times of economic distress where the cash rate may take also reached its lowest practical level. For example, in Australia the Term Funding Facility (TFF) was appear in March 2020 during the COVID-xix pandemic (see Box below on 'The Term Funding Facility').

Policies that influence the gradient of the risk free yield curve: asset purchases and forrard guidance

The risk free yield bend influences market reference rates for some sources of banking concern funding. Consequently, policies that influence its slope, such equally asset purchases and forwards guidance, may period through to depository financial institution funding costs (see Explainer: Bonds and the Yield Bend).

Other factors that influence funding costs

A diverseness of other factors can also influence bank funding costs without any change in the stance of monetary policy in Commonwealth of australia. These include:

- demand for or supply of different types of funding, for instance more competition among banks to attract deposit funding typically results in higher deposit rates

- the compensation required by savers to invest in bank debt.

What influences banks' lending rates?

Banks prepare their lending rates to maximise the profitability of lending, field of study to an advisable exposure to the chance that some borrowers will fail to repay their loans. Banks measure out the profitability of lending equally the difference between the acquirement the bank expects to receive from making the loans and the price of funding loans. Factors that affect the profitability of lending will in turn influence where a bank decides to set up its lending rates.

Banks' funding costs

Funding costs will influence where a bank sets lending rates. When funding costs modify, the response of lending rates volition depend on the expected touch on a banking company's profits. If funding costs increment, then a bank may wish to increase lending rates to maintain its profits. However, borrowers may seek to infringe less if lending rates are higher. If this were to occur, and so the banking concern would see less demand for loans and this could reduce its profits. A bank must residual these considerations in deciding how to ready lending rates.

Competition for borrowers

If borrowers are seeking to infringe less funds than banks want to lend, and so banks will have to compete to attract borrowers and maintain their profits. All else equal, a college degree of competition among banks to attract borrowers typically results in lower lending rates.

The chance that borrowers do non repay their loans

For each loan that information technology makes, a bank will appraise the gamble that a borrower does not repay their loan (that is, the credit risk). This volition influence the revenue the bank expects to receive from a loan and, as a result, the lending charge per unit it charges the borrower. If a bank considers that it is more likely to lose money from a credit carte loan than from a dwelling house loan, then the interest charge per unit on a credit menu loan will be higher than for a home loan. A bank's perception of these risks tin change over time and influence their ambition for certain types of lending and, therefore, the involvement rates they charge on them.

The Reserve Banking company announced the Term Funding Facility (TFF) in March 2020 along with several other monetary policy measures designed to help lower funding costs in the Australian banking organisation.

The TFF made a big amount of funding bachelor to banks at a very depression interest rate for three years. Funding from the TFF was much cheaper for banks than other funding sources available at the time it was announced, and that remains truthful today. (See declaration of Term Funding Facility and the Governor's speech Responding to the Economic and Financial Impact of COVID-19).

The TFF is designed to lower banks' funding costs and in turn to reduce lending rates for borrowers. The TFF also creates an incentive for banks to lend to businesses (particularly pocket-size and medium-sized businesses). This is because banks can borrow extra funding under the TFF if they increment their lending to businesses: for every dollar of actress lending to minor- or medium-sized businesses, banks tin access 5 dollars of extra funding under the TFF (for large businesses, the amount is one dollar of extra funding).

Source: https://www.rba.gov.au/education/resources/explainers/banks-funding-costs-and-lending-rates.html

Posted by: hightowerforef1989.blogspot.com

0 Response to "Where Do Banks Get Their Money From To Led To People For Loans"

Post a Comment